By Asel Mamytova, Swiss Banking & International Business Specialist | Chur, Switzerland | Updated February 2026

Every month, entrepreneurs from Dubai, Beijing, New York, and Berlin ask me the same question: “I want to open a company in Switzerland — where do I start?” Some have already spent months trying on their own and hit unexpected walls. Others assumed the process was straightforward, then discovered their application stalled at the cantonal level. A few chose the wrong legal structure and now pay significantly more in taxes than they need to.

This guide addresses all of that. You will understand why Switzerland remains one of the world’s most compelling business jurisdictions in 2026, which company structure fits your goals, how the three-tier tax system works, and which canton makes strategic sense for your business. More importantly, you will learn exactly where foreign entrepreneurs go wrong — and how to avoid those mistakes from the start.

Do you want to start a business and register a company in Switzerland? Please do not hesitate to contact us for a consultation!

Why Switzerland Still Makes Sense in 2026

The Innovation Case — Backed by Data

Switzerland topped the WIPO Global Innovation Index 2025 (GII 2025) for the fifteenth consecutive year. Out of nearly 140 evaluated countries, none displaced it from first place. The index measures 80 indicators: R&D spending, venture capital activity, high-tech exports, and patent activity. Switzerland leads in five of seven sub-indices and ranks second in innovation inputs, behind only Sweden.

For entrepreneurs, this translates into something concrete. Operating in Switzerland means working within an ecosystem where research institutions, technology companies, and the financial sector form a genuinely functional innovation cluster. ETH Zurich consistently ranks among the world’s top five universities. Novartis, Roche, ABB, and Nestlé all chose Switzerland as their global headquarters — not for the scenery, but for the talent, infrastructure, and regulatory environment.

The Tax Advantage — What the Numbers Actually Show

Switzerland’s average effective corporate tax rate in 2025 stands at 14.4%, according to the KPMG Swiss Tax Report 2025 — down from 14.6% in 2024. For comparison: Germany sits at approximately 30%, France at 25%, and Italy at 24%. Within Europe, only Hungary (9%) and Bulgaria (10%) offer lower headline rates.

The variation inside Switzerland is equally significant. The canton of Zug offers an effective combined rate of 11.85% — the lowest among all cantonal capitals. Zurich comes in at 19.61%. Bern at 20.54%. Geneva at 14.70%. In other words, choosing a canton is not an administrative formality. It is a strategic tax decision that affects your company’s profitability for years.

Double Tax Treaties and Market Access

Switzerland has signed over 100 double tax treaties (DTTs) — including agreements with the United States, the United Kingdom, China, the UAE, Germany, France, and most other major economies. As a result, income legitimately earned through a Swiss company avoids double taxation, which matters enormously for entrepreneurs operating across multiple jurisdictions.

Furthermore, Switzerland is a member of the European Free Trade Association (EFTA) and maintains 34 free trade agreements covering 44 partners worldwide. Consequently, a company registered here gains effective access to the European market of 448 million consumers — without the regulatory burden of EU membership.

The Problem Most Guides Skip Entirely

Most articles about opening a company in Switzerland treat the process as if it were uniform for everyone. It is not. Your legal status as a foreign entrepreneur determines the entire scenario. This distinction between EU/EFTA nationals and third-country nationals shapes everything that follows — and understanding it upfront saves enormous time.

If You Are an EU or EFTA National

The Agreement on the Free Movement of Persons between Switzerland and the EU grants EU/EFTA citizens essentially the same rights as Swiss nationals. You can register a company, obtain a category B residence permit, and begin operations through a straightforward process. With a complete documentation package, the entire procedure typically takes three to six weeks.

If You Are from the USA, UAE, China, or Any Other Third Country

Here is where the two scenarios diverge completely — and where most guides fail to draw the distinction clearly.

Scenario 1: You want to relocate to Switzerland and run your business from within the country.

This is where genuine obstacles arise. The Swiss Federal Act on Foreign Nationals and Integration (AIG) requires that citizens of third countries — including Americans, Chinese, Gulf nationals, and most others — obtain a category B residence permit before they can personally operate a business on Swiss soil. Cantonal authorities evaluate the economic merit of the project: job creation potential, tax contribution, and innovation value. A compelling business plan, sufficient capital, and demonstrable economic presence in the canton are all prerequisites. The review process takes two to six months, and a positive outcome is not guaranteed.

Scenario 2: You want to be a company founder and manage it remotely from your home country.

This scenario is entirely different — and for most international entrepreneurs, it is the relevant one. No restrictions on nationality exist for founders of Swiss companies. An American, Chinese, Emirati, or Saudi national can register a GmbH or AG in Switzerland, own 100% of the shares, and manage the company remotely without a residence permit or relocation. The only mandatory requirement is that at least one director holds a valid Swiss residence permit with signatory authority. This director can be a professional nominee director through a specialised firm. Therefore, for the vast majority of international entrepreneurs seeking a Swiss structure for business, holding, or tax optimisation purposes, the registration process is accessible and does not require moving to Switzerland.

Choosing the Right Legal Structure

The choice of legal structure is the first major strategic decision. Getting it wrong costs money and time. Switzerland offers three main options for foreign entrepreneurs.

GmbH (Gesellschaft mit beschränkter Haftung) — Limited Liability Company

The GmbH is the most popular structure for small and medium-sized businesses. The minimum share capital is CHF 20,000, and it must be paid in full upon registration. Liability is limited to the company’s capital, which protects personal assets.

Management is carried out by one or more managing directors (Geschäftsführer). At least one must be a Swiss resident with signatory authority. Ownership shares are not freely transferable without the consent of other shareholders, which ensures tighter control over the ownership structure. As a result, GmbH suits closely-held businesses and family structures well.

GmbH works best for: consulting firms, operational holding companies, IT and financial services, trading structures with a stable shareholder group.

AG (Aktiengesellschaft) — Joint Stock Company

The AG is Switzerland’s most prestigious legal structure and the preferred form for larger international businesses. Minimum share capital is CHF 100,000, of which at least CHF 50,000 must be paid upon registration. The remainder can follow later, though founders carry subsidiary liability for unpaid amounts.

Management is carried out by a board of directors, with at least one member holding Swiss residence. Shares can be registered or bearer; the beneficial ownership register is maintained internally and is not publicly accessible. Precisely because of this combination — limited liability, flexible share structure, and institutional credibility — the AG remains the structure of choice for international holding companies, multi-shareholder structures, and family offices.

AG works best for: international holdings, investor-ready structures, family offices, multi-shareholder companies.

Sole Proprietorship (Einzelfirma)

The simplest structure, with no minimum capital requirement. However, the owner carries unlimited personal liability for all business obligations. For non-resident foreigners, this structure is practically inaccessible — it requires permanent residence in Switzerland. It is therefore not a realistic option for most international clients.

Quick Comparison

| Criterion | GmbH | AG | Sole Proprietorship |

|---|---|---|---|

| Minimum capital | CHF 20,000 | CHF 100,000 | None required |

| Liability | Limited | Limited | Unlimited personal |

| Swiss resident director | Required | Required | N/A |

| External investors | Limited | Yes | No |

| Confidentiality | Medium | High | Low |

| For non-residents | Yes | Yes | Practically no |

Switzerland’s Three-Tier Tax System Explained

Corporate taxation in Switzerland happens simultaneously at three levels. Understanding this structure is essential before choosing a canton.

Federal Tax

The direct federal corporate income tax rate is 8.5% of taxable profit after taxes — equivalent to an effective rate of approximately 7.83% of pre-tax profit. This rate applies uniformly across all cantons.

Cantonal and Communal Taxes

This is where the meaningful differences between regions emerge. According to the KPMG Swiss Tax Report 2025, the effective combined rates (federal + cantonal + communal) by major location are as follows:

| Canton | Effective Rate 2025 |

|---|---|

| Zug (city of Zug) | 11.85% |

| Lucerne | 11.90% |

| Nidwalden | 11.97% |

| Schwyz (city of Schwyz) | 12.06% |

| St. Gallen | 14.29% |

| Geneva | 14.70% |

| Vaud | 14.72% |

| Zurich | 19.61% |

| Bern | 20.54% |

Source: KPMG Switzerland Swiss Tax Report 2025

The gap between the most favourable canton (Zug) and the highest (Bern) amounts to 8.69 percentage points. On a company profit of CHF 500,000, that difference translates to over CHF 43,000 in annual tax savings — purely from canton selection.

VAT

Companies whose annual turnover exceeds CHF 100,000 must register for VAT. Switzerland’s standard VAT rate is 8.1% — among the lowest in Europe. A reduced rate of 2.6% applies to food, books, and certain other categories.

How to Choose the Right Canton

Tax rate is important, but it is not the only variable worth considering. In practice, I advise clients to evaluate four factors together.

Tax Efficiency

If tax optimisation is the priority, Zug leads clearly. Beyond its 11.85% corporate rate, Zug also offers one of Switzerland’s lowest capital taxes — just 0.07% of taxable capital. Lucerne and Nidwalden are strong alternatives in Central Switzerland with comparable rates and lower real estate costs than Zug.

Infrastructure and Talent Access

Zurich is Switzerland’s largest financial centre, with deep talent pools in finance, technology, and professional services. Despite its higher tax rate, many international companies choose Zurich specifically for this reason. Geneva, meanwhile, provides access to the diplomatic and international institutional community, as well as a world-class banking and legal cluster — particularly relevant for Middle Eastern and Asian clients who want proximity to major private banks.

Corporate Banking Access

Opening a Swiss corporate bank account is a separate process from company registration — and a challenging one in its own right. The proximity to banking centres in Geneva or Zurich matters practically. I work with clients on both processes simultaneously, coordinating company registration and corporate bank onboarding to avoid the delays that arise when these two tracks fall out of sync.

Graubünden and Chur

For small and medium-sized businesses that do not require immediate access to major financial markets, Chur — the capital of Graubünden canton — offers a practical combination of moderate taxes, high quality of life, and lower operating costs than Zurich or Geneva. I live and work here, which gives me genuine insight into the local business environment from the inside.

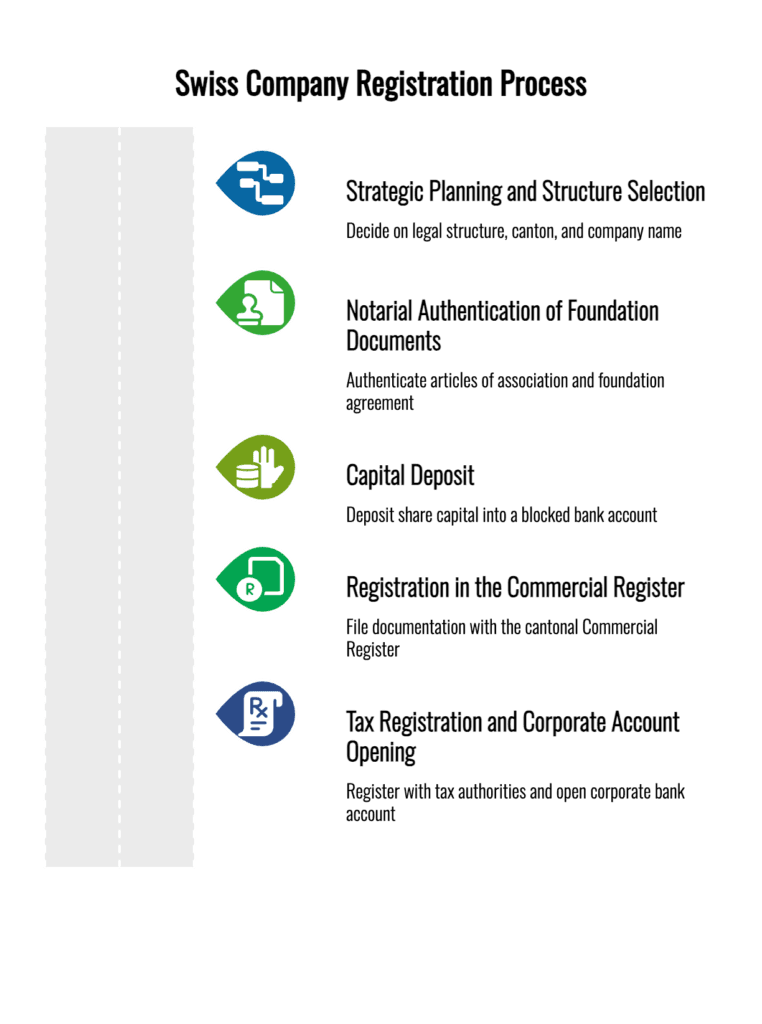

The Step-by-Step Registration Process

Understanding the process before you begin saves weeks and prevents the most common documentation errors.

Step 1: Strategic Planning and Structure Selection

First, decide on the legal structure and canton — these are interdependent decisions. Simultaneously, verify your chosen company name against Switzerland’s commercial register. The name must be unique and must not mislead about the nature of the business. Additionally, resolve the resident director requirement at this stage if you do not hold a Swiss residence permit yourself.

Step 2: Notarial Authentication of Foundation Documents

Swiss law requires notarial authentication of the articles of association and foundation agreement. For foreign founders, this means either personal presence or a notarised and apostilled power of attorney. All documents must be in the official language of the chosen canton — German, French, or Italian.

Step 3: Capital Deposit

The share capital is deposited into a blocked bank account before registration. The bank holds these funds until the company receives its registration certificate. This step creates a practical coordination challenge: opening a bank account for a non-resident requires separate preparation and time. I help clients synchronise both processes to prevent delays.

Step 4: Registration in the Commercial Register

After notarial authentication, the documentation is filed with the cantonal Commercial Register. The registration period typically takes three to four weeks with a complete documentation package. Upon registration, the company receives its unique IDE number (enterprise identification number).

Step 5: Tax Registration and Corporate Account Opening

Following registration, the company must register with cantonal tax authorities. If annual turnover will exceed CHF 100,000, VAT registration is also required. Simultaneously, the permanent corporate bank account needs to be opened — a separate compliance process that runs in parallel.

Opening a Swiss Corporate Bank Account: The Hidden Challenge

Many entrepreneurs are surprised to discover that company registration and corporate bank account opening are two completely independent processes in Switzerland — each requiring its own compliance review.

Swiss banks apply the same rigorous KYC standards to corporate clients as to private ones. The compliance team examines: the ownership structure and beneficial owners, the source of the share capital and operating funds, the nature of the company’s activities and geographic transaction flow, and the reputational profile of directors and shareholders.

As a result, you should begin preparing bank documentation simultaneously with company registration — not after. A delay at this stage can block the company’s operational activity for months, even with a valid registration certificate in hand. For clients from the Middle East, China, and the United States in particular, this process requires careful preparation given the enhanced due diligence these jurisdictions typically trigger in Swiss banking compliance.

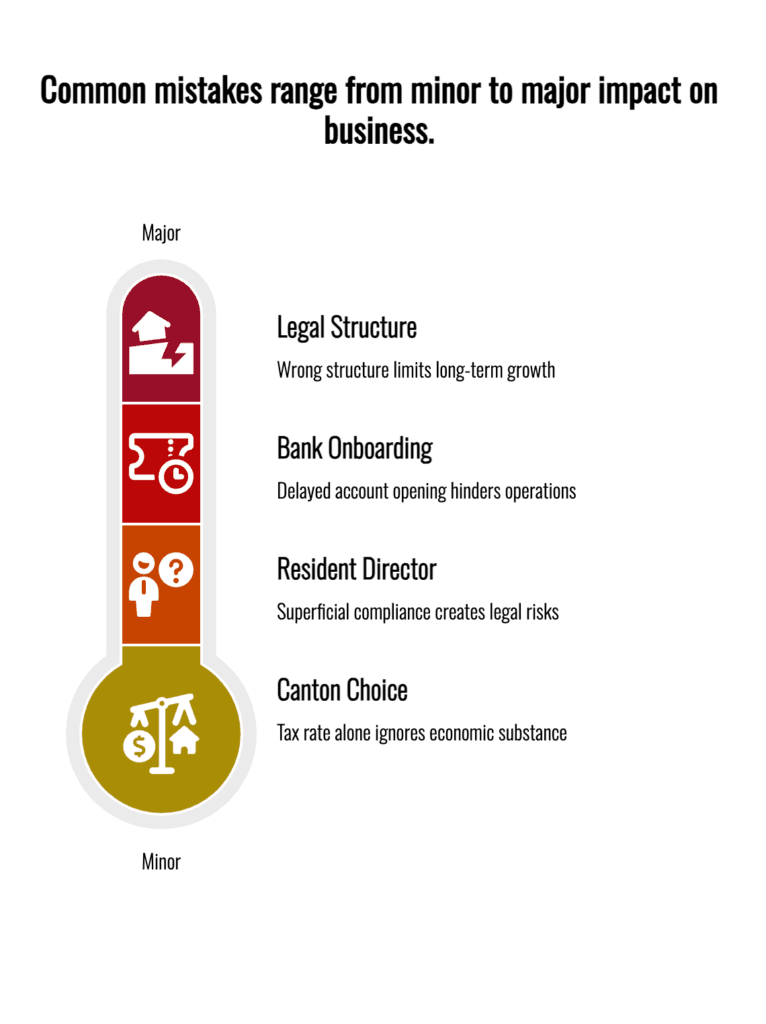

Common Mistakes That Cost Foreign Entrepreneurs Time and Money

After years of working with international clients on Swiss company structures, I see the same errors repeatedly. Avoiding them upfront makes a meaningful difference.

Choosing a canton based solely on tax rate. Zug is undeniably attractive. However, if your company lacks a genuine presence in the canton — a real office, employees, business activity — cantonal tax authorities can challenge the company’s residency. Tax planning must combine with real economic substance.

Underestimating the resident director requirement. The rule that at least one director must be a Swiss resident is not a formality. Superficial compliance — a nominal director with no real involvement in management — creates legal and tax risks over time. The director must be reachable, properly documented, and genuinely part of the governance structure.

Separating company registration from bank onboarding. I see this constantly: the company is registered, but there is no operational account for three or four months. Bank documentation preparation must begin in parallel with registration — not sequentially.

Choosing the wrong legal structure. A GmbH with CHF 20,000 in capital and a structure that cannot accommodate external investors will limit growth later. Conversely, an AG with CHF 100,000 for a small consulting operation is unnecessary overhead without real benefit. The structure must match the long-term strategy, not only the immediate requirements.

Switzerland vs. Other European Jurisdictions

| Criterion | Switzerland | Germany | Netherlands | Luxembourg | UAE (DIFC) |

|---|---|---|---|---|---|

| Average corporate tax | 14.4% | ~30% | ~25% | ~24% | 9% |

| Innovation rank (GII 2025) | 1st | 11th | 8th | — | — |

| DTT network | 100+ treaties | 90+ | 90+ | 80+ | 130+ |

| Currency stability | CHF (exceptional) | EUR | EUR | EUR | AED (pegged) |

| Minimum capital (LLC) | CHF 20,000 | EUR 25,000 | EUR 0.01 | EUR 12,000 | AED 50,000+ |

| EU market access | Via EFTA | Direct | Direct | Direct | Limited |

Practical Takeaways: Where to Begin

Start by establishing your legal position — EU/EFTA national or third-country national. That single distinction shapes the entire timeline and the realistic scope of what is possible.

Next, choose your legal structure based on capital size, shareholder composition, and investor plans. In parallel — not sequentially — select the canton, identify the resident director, and begin preparing for bank onboarding.

If you want to avoid the mistakes described above and complete the registration correctly the first time, feel free to reach out to me directly. I live and work in Chur, understand the Swiss business environment from the inside, and help international clients navigate the full process — from canton selection and legal structure to corporate bank account opening. Proper preparation cuts the entire timeline in half.