Opening a Swiss bank account remains one of the most respected financial moves for internationally active individuals. However, in 2026 the process is significantly more compliance-driven than many outdated guides suggest.

Swiss banks today operate under strict AML, CRS, and risk-based onboarding frameworks. As a result, foreign applicants are evaluated far more carefully — but with the right preparation, approvals remain very achievable.

During my 10+ years working directly with foreign high-net-worth clients, I have seen both successful openings and repeated rejections. The deciding factor is almost never luck. It is preparation, transparency, and understanding how Swiss banks actually assess risk.

In this updated guide, I will share the pillar principles that materially increase your chances to open a Swiss bank account in 2026, highlight real problems clients face, and demonstrate how properly structured applications succeed.

Would you like to open bank account for non-resident at reputable Swiss bank, or a private bank in Singapore, Liechtenstein or Monaco? Read our guideline how to open a swiss bank Account as a foreigner

Swiss Banking in 2026: What Has Changed

Over the past few years, Swiss banks have further strengthened their onboarding controls due to:

- tighter FINMA supervision

- expanded CRS data exchange

- enhanced AML monitoring systems

- increased geopolitical risk screening

- AI-assisted transaction and client risk scoring

Important reality: Switzerland remains open to foreign clients — but banks are far more selective and documentation-focused than a decade ago.

Why Swiss Banks Still Attract International Clients

Despite stricter compliance, Switzerland continues to be a premier jurisdiction because of:

- exceptional banking stability

- advanced wealth management expertise

- strong investor protection culture

- multi-currency infrastructure

- political neutrality

For internationally mobile entrepreneurs and investors, the Swiss banking ecosystem remains highly valuable — provided the onboarding is handled correctly.

How Swiss Banks Evaluate Foreign Applicants (2026 Model)

In 2026, most Swiss banks use multi-layer AML risk scoring models. While methodologies differ between institutions, the core evaluation pillars remain consistent.

1. Client Nationality

Nationality influences baseline risk scoring through:

- FATF country classification

- sanctions proximity

- corruption perception metrics

- historical compliance data

Key insight: Nationality alone rarely leads to rejection — but it often determines the depth of due diligence.

2. Country of Tax Residence

This factor has become even more important in 2026.

Banks assess:

- CRS reporting clarity

- tax transparency

- economic substance

- consistency between residence and income source

⚠️ Red flag: When clients live in one country but generate income primarily in unrelated higher-risk jurisdictions without clear explanation.

3. Business Activity Risk Profile

This is frequently the decisive element.

Swiss banks analyze:

- industry classification

- revenue model transparency

- geographic exposure

- client base composition

- expected transaction flows

Industries now receiving enhanced scrutiny in 2026 include:

- cross-border IT services

- crypto-related activities

- online marketing and affiliate models

- high-volume trading

- complex consulting structures

Again — these are not automatic rejections. They simply require stronger positioning.

The Most Common Problems Foreign Clients Face

Based on a decade of practical work, the same patterns appear repeatedly.

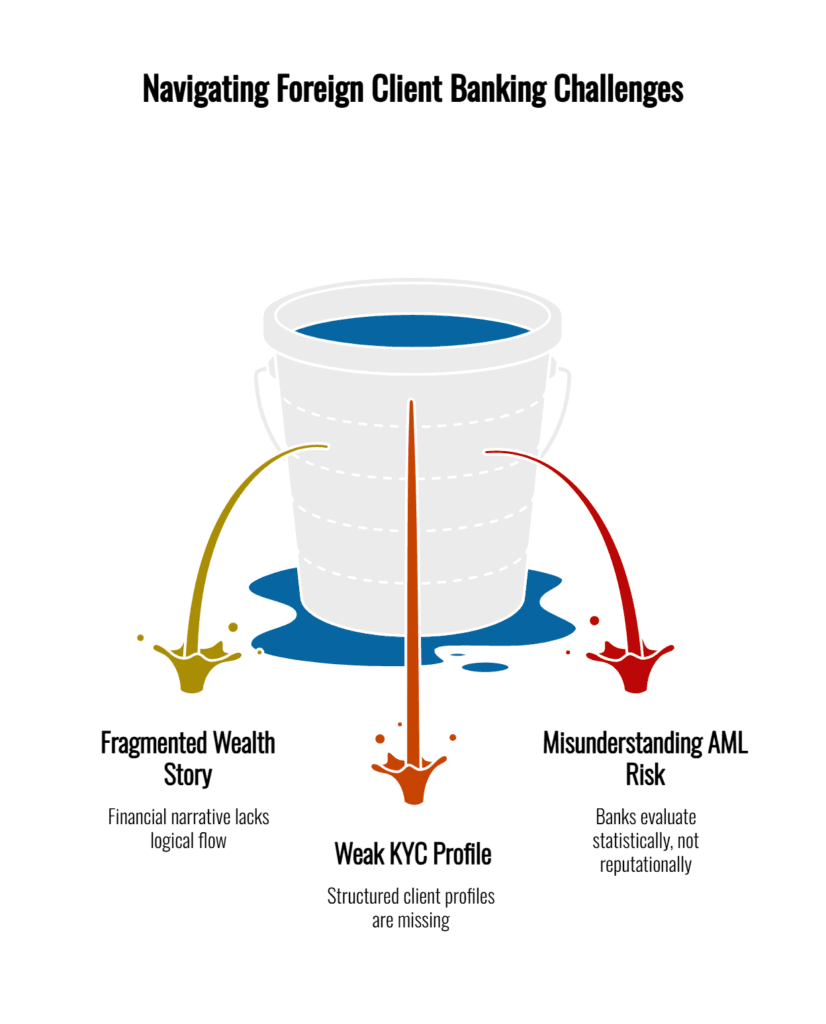

❌ Problem 1: Fragmented Wealth Story

Many clients provide documents, but the financial narrative does not logically connect.

Swiss compliance teams think in structured flow:

income → taxation → accumulation → current assets

If this chain contains gaps, the application risk score increases immediately.

❌ Problem 2: Weak or Generic KYC Profile

In 2026, banks expect highly structured client profiles.

Typical weaknesses I still see:

- unexplained international flows

- vague business descriptions

- missing counterparty explanation

- unclear beneficial ownership

- inconsistent revenue figures

❌ Problem 3: Misunderstanding AML Risk Perception

Many legitimate clients are surprised by rejections because they evaluate themselves reputationally, while banks evaluate statistically.

Swiss institutions rely heavily on automated and manual risk scoring, not personal impressions.

Real Case Study (2025–2026): IT Entrepreneur from CIS Region

To demonstrate how proper structuring changes outcomes, here is a real anonymized case from my recent practice.

Initial Client Situation

Client profile:

- Nationality: CIS country

- Tax residence: different jurisdiction

- Business: international IT services

- History: rejected by multiple Swiss banks

Despite being fully legitimate, the client triggered elevated AML scoring due to:

- geographic exposure

- industry sensitivity

- unclear wealth timeline

- inconsistent supporting documents

Our Strategic Solution

Instead of resubmitting blindly, we rebuilt the application using a compliance-first methodology designed for the 2026 banking landscape.

Structured Wealth Journey

Document Harmonization

Cash Flow Intelligence

Professional KYC Narrative

Risk Perception

Improved Materially

Due Diligence

Smooth Progression

Timeframe

Approx. 2 Months

Institution

Top-Tier Swiss Bank

Understanding AML Risk Scoring in 2026

Swiss banks now combine high-velocity tech with deep manual scrutiny.

Geographic Risk

Nationality + actual tax residence + business footprint.

Industry Risk

Business model viability and sectoral AML sensitivity.

Flow Behavior

Expected transaction volume vs. actual corridor frequency.

Source of Wealth

Verifiability of asset accumulation over the last 10+ years.

Documentation Quality

Internal consistency across all submitted corporate records.

Transparency

Clarity of explanations for complex economic purposes.

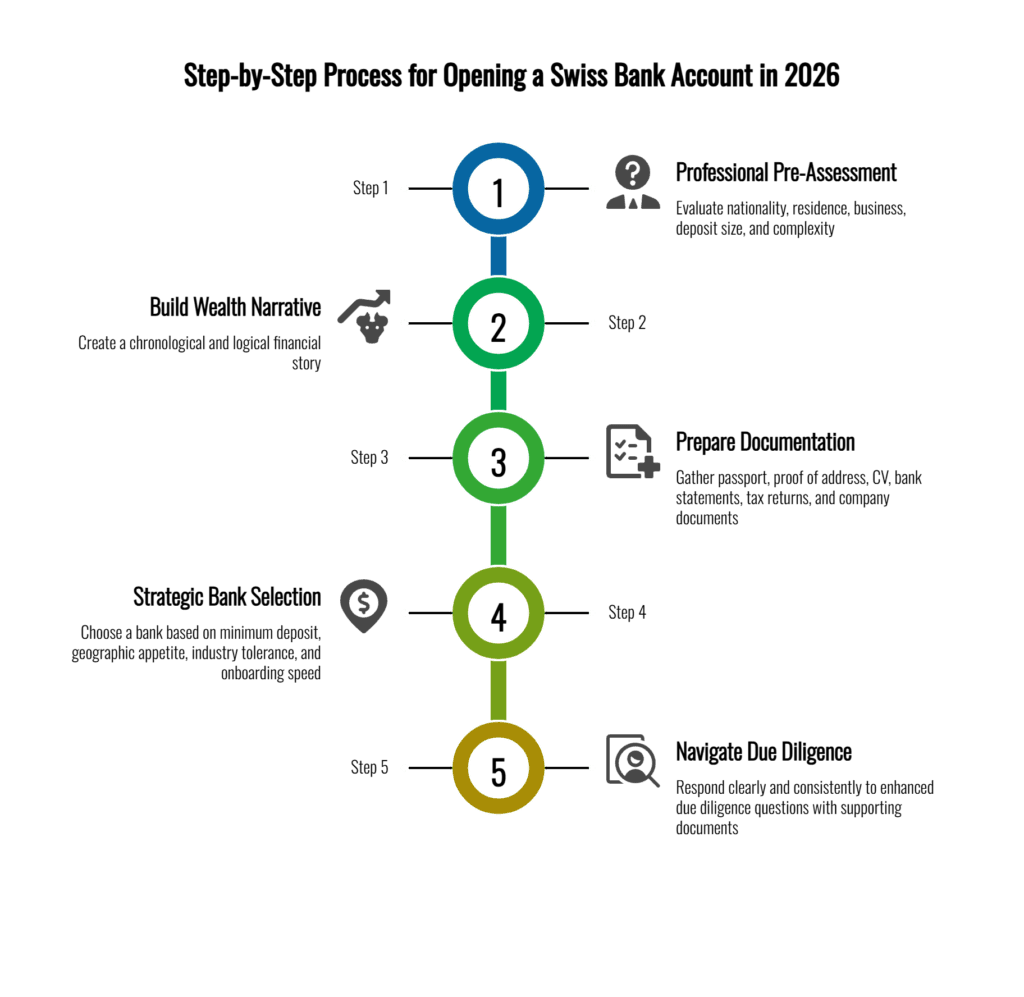

Step-by-Step: How to Open a Swiss Bank Account in 2026

Based on current banking practice, this process yields the highest success rate.

Step 1 — Professional Pre-Assessment

Before contacting any Swiss bank, evaluate:

- nationality risk level

- residence jurisdiction

- business industry

- expected deposit size

- structural complexity

This step alone can prevent most rejections.

Step 2 — Build a Coherent Wealth Narrative

Your financial story must be chronological and logical.

You must clearly demonstrate:

- current banking relationships

- how wealth was generated

- where taxes were paid

- how assets accumulated

Step 3 — Prepare High-Quality Documentation

Typical requirements in 2026 include:

- passport

- proof of address

- detailed CV

- recent bank statements

- tax returns or confirmations

- company documents (if applicable)

- contracts or invoices

- sometimes source-of-wealth memo

Quality and consistency now matter more than ever.

Step 4 — Strategic Bank Selection

Swiss banks differ significantly in:

- minimum deposit thresholds

- geographic appetite

- industry tolerance

- onboarding speed

- private vs retail focus

Random bank applications often fail. Targeted positioning works.

In 2026, expect deeper questions than in the past.

Best practice:

- respond clearly

- remain consistent

- support statements with documents

- avoid vague explanations

Most delays occur due to incomplete answers.

How Nationality, Residence, and Business Type Interact

Swiss banks evaluate combined risk exposure, not isolated factors.

Practical Risk Matrix

| Factor | Lower Risk Profile | Higher Scrutiny Profile |

|---|---|---|

| Nationality | Western Europe | higher-risk regions |

| Residence | Switzerland/EU | offshore mismatch |

| Business | consulting | complex cross-border IT |

| Transactions | predictable flows | high-velocity multi-jurisdiction |

A strong profile in one area can compensate for another — but weak combinations trigger enhanced review.

Expert Tips From 10+ Years Working With Foreign HNW Clients

These principles consistently improve approval probability:

- Be radically transparent

- Ensure tax consistency

- Explain international exposure clearly

- Structure documents professionally

- Avoid cold, unprepared bank approaches

- Align your wealth narrative before applying

Who Can Successfully Open a Swiss Bank Account in 2026?

Regardless of total wealth, incomplete documentation leads to automatic rejection in 2026.

Final Thoughts

In 2026, opening a Swiss bank account as a foreign client is absolutely achievable. However, the process has evolved into a highly structured compliance exercise.

After more than a decade working with international HNW clients, one pattern remains consistent:

Swiss banks rarely reject good clients — they reject unclear stories.

If your application demonstrates:

- a coherent wealth journey

- properly aligned documentation

- transparent tax position

- and professional KYC structuring

your chances of approval increase significantly.

Next Step

If you want to open a Swiss bank account with maximum probability of success, the smartest first move is a professional pre-assessment of your profile before approaching any bank.

This prevents unnecessary rejections and positions your application exactly how Swiss compliance teams expect to see it.